A Recession is Exactly What We Need and it’s Good for Housing

As March wrapped up, the two-to-10-year treasury yields had a .05% spread, and they are on the verge of inverting, which is a high validity recession indicator. Five of the last six recessions were preceded by an inversion. However, today we also have an incredibly strong labor market as the unemployment rate just fell to a post-pandemic low of 3.6%. In fact, unemployment has only been lower than 3.6% three times since 1950. Nonfarm payroll saw a robust 431,000 jobs added and with 11.3 million job openings, and the labor force participation rate inched back up to 62.4%, a post-pandemic high. Incomes also had a lift, rising .4% month-over-month and 5.6% over the last 12 months nationwide. Denver came in stronger at 5.81%.

With a strong labor market, is the two-to-10-year treasury yield a worthwhile indicator? I think it is especially when you couple it with the unemployment indicator. Every time there has been a recession, the unemployment rate comes off a bottom and starts to tick up. When the economy contracts, businesses look to lower spending to adjust to lower revenues, which leads to layoffs and rising unemployment. Think about our current market. We had record-high quits with 4.4 million workers leaving their position in February and looking for higher paying jobs. Labor accounts for as much as 70% of total business costs. Those employees are looking to offset rising inflation as the Fed’s favored Personal Consumption Index (PCE) was just released for February at a 40-year high of 6.4%. February’s Consumer Price Index (CPI), or the index which measures what you and I feel daily, was a higher 7.9%.

The cost of everything Americans buy is high, and employment is available for all those who want it. These are the only two mandates Fed Chair, Jerome Powell, and his board have. Their focus must turn towards managing inflation. It has gone well past transitory. They have announced seven more increases, one of which one might be 50 BP, with a goal of the Fed Rate reaching 2% by end of 2022 and 3% by end of 2023. The most recent PCE release has the market believing we will see a 50 BP increase during the next two meetings as Powell speeds up the Fed’s action.

So, inflation is high, the Fed Rate is rising, unemployment is low, job openings are abundant and supply chains continue to be exacerbated by a pandemic and now a war.

What does this mean for housing?

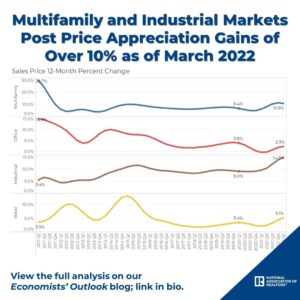

Home prices, much like other consumer goods and services, continue to be pressured by supply chain constraints. CoreLogic last reported a 20.8% annual rise in Denver home prices, with a cumulative gain of 30.5% since the start of the pandemic. DMAR’s March data reflected a median closed price growth of 20.55% and an average of 19.88%. Days in the MLS continue to be a blip of only four days for an average close-to-list of 106.46%. The price of everything clearly includes housing and homeowners and sellers are on the winning side.

Active listings jumped by almost 1,000 units as buyers saw interest rates move from 3.9% on March 1 to 4.78% on March 31. There was a similar increase in inventory in 2018 when rates pushed above 5%. In March, there were 1,827 new listings that came on the market, a 44% month-over-month increase. More than half of these new listings were scooped up as pending listings increased by 1,039 and closed listings increased by 941. While more inventory might give buyers a little breathing room, they are not slowing down. With more inventory, we have more sales.

This additional inventory is partially due to seasonality. Some of it is investors taking their winnings off the table. Others are looking at this intense demand and talks of a bubble and wanting to play the timing game. I think as prices rise, high prices will be the cure for high prices. The appreciation, much like inflation, will slow down; however, talks of a bubble assume high prices are the tipping point. They aren’t. Homeownership equity is 69.2%. A vacancy rate of 1.6% and a high birthrate 30 to 33 years ago all starve off the bubble talks. A $75,000 annual equity gain for an average Coloradoan, in addition to a .01% Colorado foreclosure rate and a 1.9% 30-day late rate, tells me struggling homeowners don’t have to sell at a discount, just at market.

These prices and rates impact all buyers, especially first-time homebuyers. Mortgage purchase applications are down 10% from last year when a median home in Denver’s metro cost 20% less and a buyer could lock in an interest rate of 3.37%, 1.4% lower than what it is today. That P&I difference is $757 a month. While wages are going up, they are not enough to offset the rising cost of everything.

So, what’s the answer?

Buy and buy now. I know it’s not easy, but home prices will continue to go up. Hopefully, appreciation will slow as more inventory comes online and rates continue to rise. Lock in today’s home price at today’s interest rate because a recession is probably coming. I say “probably” because economic indicators tell us it is, but forecasters have only been able to recognize we are in a recession once we’re in one. A recession does not equal a housing bubble. In fact, during all of the recessions, except for 2008, housing increased in value as interest rates declined with a slowing economy. So, buy now, refinance then, and build equity and stability between now and then because the alternative is paying 15.5% more in rent.

That’s a wrap for this month’s Market Trends Update. It’s my pleasure to keep you updated,

Nicole Rueth

Producing Branch Manager with The Rueth Team of Fairway Mortgage

Source: https://www.dmarealtors.com/